Amazon and Wal-Mart; Atypical Market Rally Driven by Disintermediation and Secular Trends

Wal-Mart recently hosted an Analyst Day to update Wall Street on current operating trends and strategy. The amount of investment needed to modernize the store base, and improve the overall customer offering is staggering. Wal-Mart will experience a second consecutive year of earnings decline in 2016. The stock took the update poorly, falling over 12% from last week’s price of $67 to $58 on Friday. The decline slashed $27b in market capitalization. Along with Wal-Mart, the retail sector got pounded, despite a rampaging market and stunning moves within large-cap tech.

Wal-Mart recently hosted an Analyst Day to update Wall Street on current operating trends and strategy. The amount of investment needed to modernize the store base, and improve the overall customer offering is staggering. Wal-Mart will experience a second consecutive year of earnings decline in 2016. The stock took the update poorly, falling over 12% from last week’s price of $67 to $58 on Friday. The decline slashed $27b in market capitalization. Along with Wal-Mart, the retail sector got pounded, despite a rampaging market and stunning moves within large-cap tech.

While the market isn’t at new highs (yet), the August sell-off is now undone, and the market trades solidly within the range of the previous 7-months (2,050-2,130). What’s going on? The current rally is atypical because it’s driven by two factors:

1) Policy/stimulus on a global basis

2) Select companies with superior business models with the power to disintermediate

Wal-Mart is a good example because the company is large and well known. Wal-Mart was created for a different era, pre-internet. A legacy cost structure assumed certain behavioral norms from the US consumer, such as willingness to invest time driving to, and shopping in, large box stores. Wal-Mart was conceptualized by the folksy Sam Walton, who maniacally focused on the customer service that was relevant during his era. Wal-Mart worked for decades, crushed inefficient competitors, and gained market share.

Today, Wal-Mart faces challenges because the business model is now sub-optimal. In order to compete with Amazon online, Wal-Mart is trying to become more technology focused and commencing a massive investment cycle. Technology investment may or may not pay off. Moreover, the legacy costs of the old business model in the form of wages and leases remain in place and move higher. This year and next year Wal-Mart is lifting associate wages to a minimum of $9 and $10 per hour respectively. With sales under pressure from online competition, and costs/investment moving higher, earnings are on the decline and the stock price is sinking.

On the other hand, Amazon was conceptualized in the internet era by a brilliant founder, the company lacks a store base and associated lease obligations, and is not labor intensive. Wal-Mart is the largest employer in the US with over 2.2m employees while Amazon employs 110,000. Wal-Mart employs more than 20x the people Amazon does yet sales are only about 4.5x larger. The lease obligation of the two companies isn’t comparable.

Disintermediation is leading to an atypical market dynamic. Generally, the mid-cycle of an economic expansion leads to broadening gains as confidence grows and the outlook within several sectors improves. This broad strength isn’t translating in a typical way because of the pace of technological change and market share shifts. Wal-Mart’s business model isn’t the only one under assault, all of US retail is. Another example is the spectacular gains of Google relative to the pressure on the traditional cable model based on “cord cutting”. Google’s stock is outperforming the cable sector and Disney (ESPN) this year.

The above missive is simply an observation, but germane to the market outlook. While the market has recovered greatly, there continues to be a ravishing bear market for dated business models or market share donors without visibility to modernize quickly. Impressive earnings from stocks like Amazon and Google are more reflective of the pace of behavioral shifts as opposed to a rising tide throughout the global economy. Valuations awarded to the winners can’t be too high, while losers see relentless valuation compression. Market leadership is narrow and overall valuations are high (once again) so risks remain elevated, and stock selection is paramount.

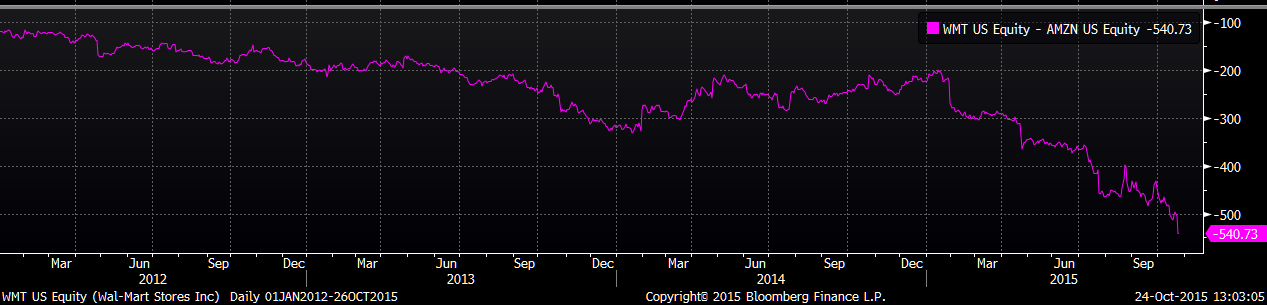

Wal-Mart stock price relative to Amazon since 2012:

- Investment in AMZN in 2012 is worth 3.4x more than investment in WMT.

How do you think Walmart will do in the cell phone market this holiday season perhaps you should pick one up and see how to use. I predict massive price wars this holiday season consumers will be licking their chops

CJF, perhaps your finest posting as yet. Congratulations. It’s out of the immediate scope of your column as a whole, but the comparable employment figures between Walmart and Amazon lead to another discussion that gets to a subject no less vital than the the future of capitalism. What is going to happen when amazon and other internet based businesses with very few employees eventually put traditional competitors with a high number of employees out of business. Putting aside for the moment the debate over good jobs versus bad jobs and focusing simply on the number of jobs, we’ve got issues. There was an interesting piece in the Guardian over the summer about the future of capitalism in the sharing economy. Of course, the Guardian is rooting for the end of capitalism but it makes some good points. And, to make another point, aside from the future viability of capitalism as we know it, startups and companies with disruptive technologies are not going public, changing the face of capitalism. Perhaps, when you have time, you could take on some of these meaty subjects. Because the world wants to know what CJF thinks about such things.

Thanks Kid Chowda – feedback is always welcome. There are indeed profound shifts within the labor market, and the notion that kids will have it better off than parents, just based on, well, “progress”, appears dubious….

Other than computer programmers and software engineers many typical “good” jobs are more highly regulated and/or in industries with profit pool issues.

I’ll attempt to cover this subject in real time as news and interesting items come up from corporate earnings and economic reports.

CJ